Categories

Home Buying, Market StatusPublished April 29, 2025

Mortgage Rates Are on a Roller Coaster—Here’s What You Can Control

Have you seen where mortgage rates have been lately? One day they dip, the next day they bounce right back up. If you’re trying to decide whether now’s a smart time to buy a home, it can feel like trying to hit a moving target.

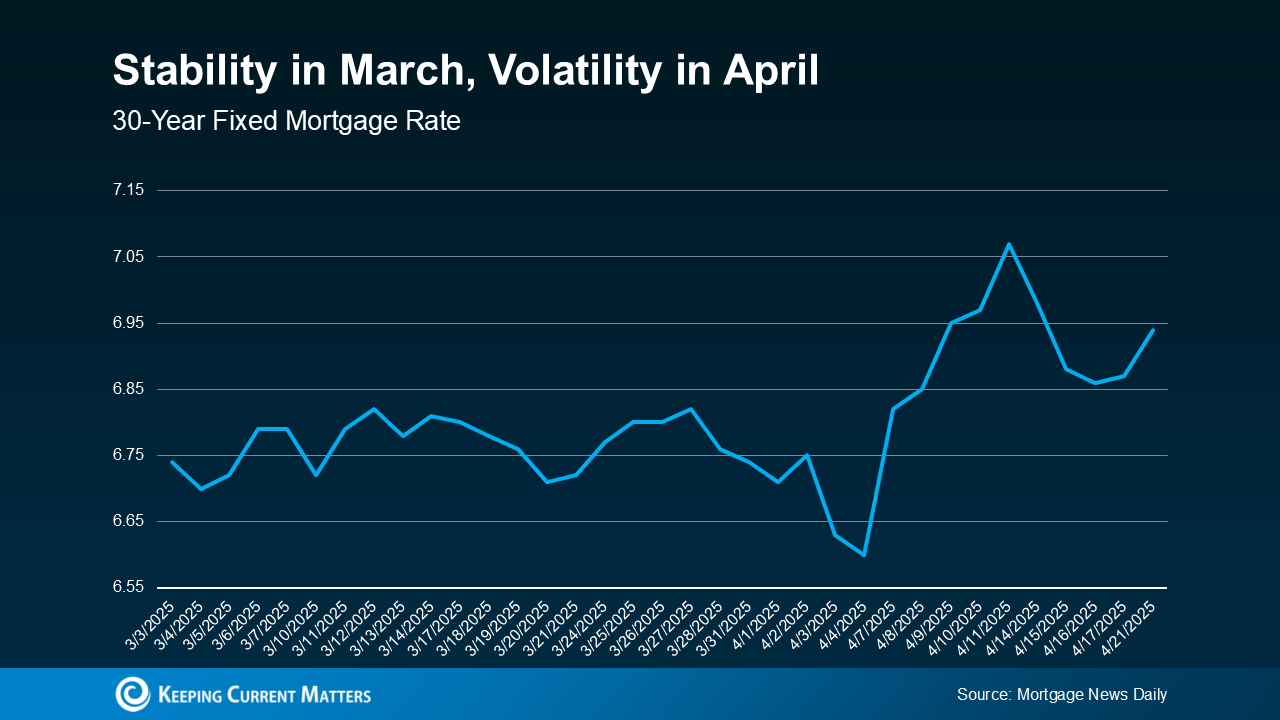

Just take a look at recent data from Mortgage News Daily. After a relatively stable March, April has been all over the place when it comes to rates—proof that we’re in a season of economic volatility. And when the economy shifts, mortgage rates often follow suit.

This back-and-forth is one of the main reasons I always caution buyers against trying to “time the market.” The truth is, we don’t get to control what the economy does next. But here’s what we do get to control—you. More specifically: your credit score, your loan type, and your loan term.

Let’s break that down:

✅ Your Credit Score Matters More Than You Might Think

Your credit score plays a big role in the mortgage rate you qualify for. Even a small bump in your score can mean real savings over the life of your loan. As Bankrate puts it:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage… Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

If you’re not sure where your credit stands—or how to improve it—talk to a local loan officer you trust (need a recommendation? I’ve got some great ones).

🏡 Not All Loans Are Created Equal

There’s more than one path to homeownership, and the loan you choose can have a major impact on your interest rate. According to the Consumer Financial Protection Bureau (CFPB):

“Rates can be significantly different depending on what loan type you choose.”

From conventional to FHA, VA, or USDA loans, each one has its own perks and eligibility requirements. I always recommend talking to a few lenders so you can compare your options.

📆 The Loan Term You Pick Affects More Than Just Your Monthly Payment

You’ve probably heard of 30-year loans, but there are also 15- and 20-year options—and each one affects your rate, payment, and long-term costs differently. Freddie Mac explains:

“Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

The “best” term really depends on your goals, your timeline, and your budget.

The Bottom Line from Laura

You may not be able to predict where rates will be tomorrow, next month, or next year—but you can take steps now to set yourself up for success.

If you’re thinking about buying and want to talk strategy, I’m here to help you make a smart move—no matter what the market's doing.

Sources:

-

Mortgage News Daily

-

Bankrate

-

Consumer Financial Protection Bureau (CFPB)

-

Freddie Mac

Laura Smith

Agent/Owner | Laura Smith Real Estate Team | Keller Williams e-Edge

or another way