As mortgage interest rates track the Fed’s benchmark rate lower, borrowers can expect an added benefit from lenders trimming the premium they have been charging to cover the risk of refinancing. “The spread will narrow,” Wachter said. “There’s a double positive in our future for borrowers.”

Published December 15, 2023

Navigating the Dynamic Landscape of Mortgage Rates: Laura’s Insights and Explanation of Trends

Need some good news about the real estate market? I think we all need some hope that in 2024 we will see things level out. If you find all this kind of information boring, at least do me the favor of scrolling to the bottom to see the conclusion

Navigating the Dynamic Landscape of Mortgage Rates: Laura’s Insights and Explanation of Trends

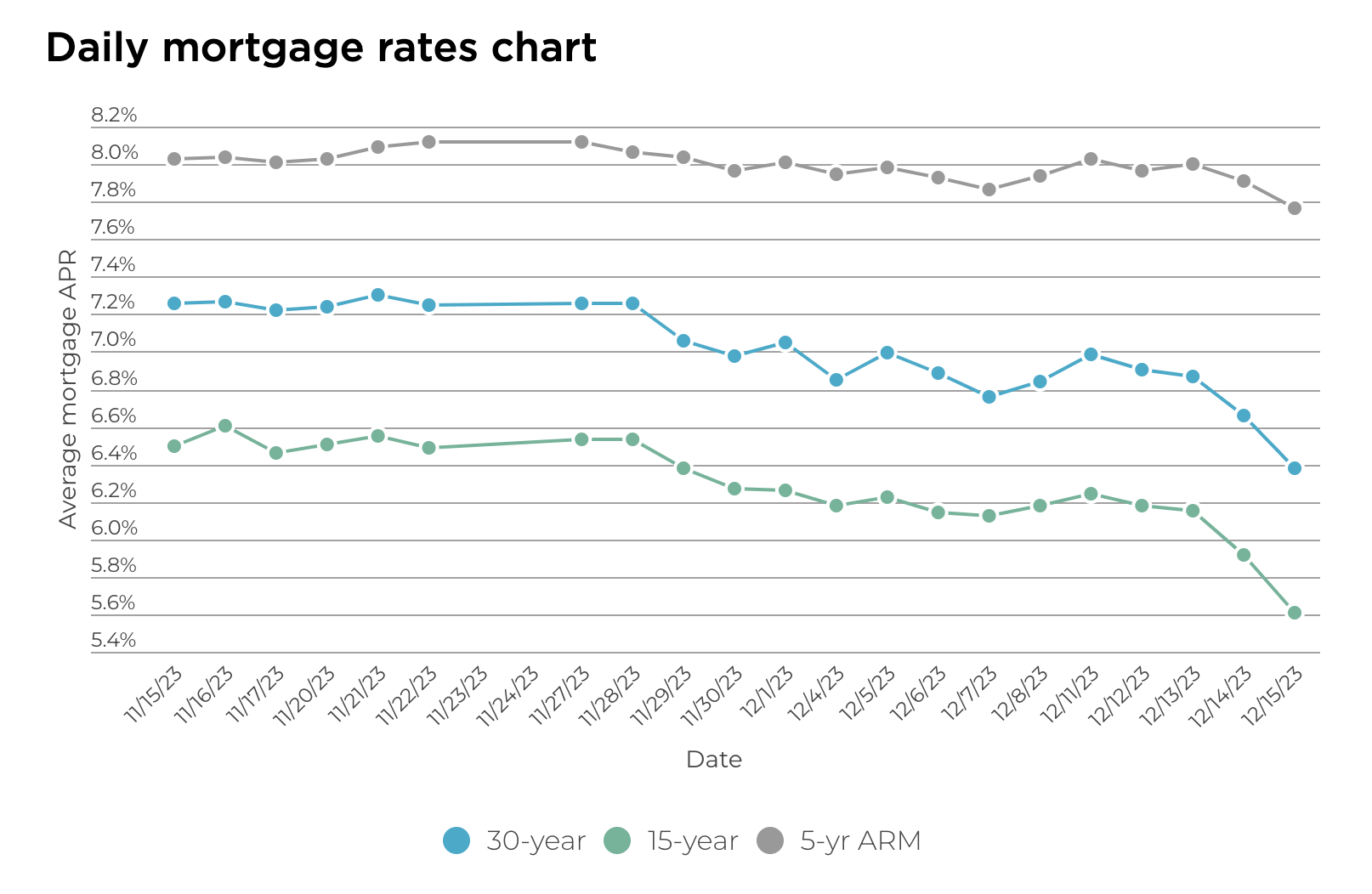

In the ever-changing landscape of the real estate market, staying informed about mortgage rates is crucial for both aspiring homebuyers and current homeowners. As of Friday, December 15, 2023, mortgage rates have experienced significant fluctuations, and we are finally seeing a glimpse of potential relief for those trying to navigate the challenging housing market. This is the lowest we have seen rates in over 4 months! Hallelujah, affordability is making a comeback!

Current Mortgage Rates:

According to data provided by Zillow to NerdWallet, on December 15, 2023, the average interest rates witnessed notable changes. The 30-year fixed-rate dropped by 29 basis points to 6.375% APR, the 15-year fixed-rate fell by 32 basis points to 5.606% APR, and the 5-year adjustable-rate mortgage decreased by 14 basis points to 7.763% APR1.

The dynamic nature of mortgage rates is evident in the continuous fluctuations, driven by factors such as inflation expectations, job creation, and overall economic growth. Generally, rates rise with a strengthening economy and fall during periods of economic decline1.

Personalized Interest Rates:

You'll almost certainly end up with a different interest rate than you'll see quoted on mortgage lenders’ websites. The reason is that your rate will be personalized according to your circumstances. The rates advertised on websites usually assume that you're using the loan to buy a primary home, that it's a single-family house, that you're making a substantial down payment, that you're paying closing costs out of pocket and that regulators consider it affordable.

If your circumstances differ, the interest rate will, too — for example, if you're refinancing instead of buying a home, or it’s a condominium instead of a house, or you're making a down payment of less than 20%, or you're rolling some of the closing costs into the loan amount, or the monthly payments will take a bigger-than-usual bite of your income.

The lender will gather these details when you apply for mortgage approval and will provide an estimate of a personalized rate.

Advertisements often assume a credit score of 740 or higher. If your credit score is lower than that, the interest rate might be higher.

Credit Score Impact:

Your credit score significantly influences your mortgage interest rate, following a concept known as "risk-based pricing." Higher credit scores translate to lower risks for lenders, leading to more favorable interest rates. Conversely, lower credit scores may result in higher interest rates1.

Mortgage Rate Locks:

A mortgage rate lock is a crucial aspect of the home buying process, providing a guarantee from the lender that the agreed-upon interest rate will remain unchanged until the specified deadline for closing. It's advisable to lock in a rate when comfortable with the monthly payments at that particular interest rate1.

Current Market Conditions:

Amidst the challenging housing market, relief is on the horizon. Borrowing costs for 30-year fixed-rate mortgages recently dropped below 7 percent after peaking at 7.8 percent just six weeks prior1. The Federal Reserve's decision to pause interest rate hikes has provided optimism, indicating a potential improvement in the housing outlook1.

Future Expectations:

The trajectory of mortgage rates is closely tied to the Federal Reserve's actions. While most economists anticipate rate cuts in the first half of the coming year, the timing of these reductions translating into cheaper mortgages remains uncertain1. The Mortgage Bankers Association projects a potential decrease in the interest rate on 30-year mortgages to 6 percent by the end of next year1.

Impact on Home Affordability:

But even as borrowing costs edge down, many current homeowners may remain unwilling to list. More than 82 percent of current homeowners have locked in mortgages with rates below 5 percent, according to Redfin data. Daryl Fairweather, the site’s chief economist, projects that listings will pick up next year, outstripping demand and causing home prices to fall by 1 percent.

How did we get here?

The pandemic sent the housing market into overdrive, as Americans who were flush with cash and encouraged by low borrowing costs rushed to buy homes. Median home-sale prices surged by roughly 50 percent from the start of the pandemic to the end of last year, according to Fed data.

It wasn’t just real estate that overheated. Prices spiking across the economy prompted the Fed in the spring of 2022 to start raising interest rates in a bid to get inflation under control.

The effort has largely succeeded. Inflation has moderated, with prices climbing 3.1 percent in November over the previous year, down from a high of 9.1 percent in June 2022. But the Fed’s campaign has also helped foster the real estate conditions pushing would-be buyers back onto the sidelines.

Conclusion:

Navigating the intricacies of mortgage rates requires an understanding of market trends, individual circumstances, and the broader economic landscape. As you move forward, having a trusted real estate advisor and staying informed about these factors is essential for making informed decisions in the dynamic world of real estate. I have been in real estate 17 years, 10 of those as an agent myself. I have seen the market shift, interest rates hit an all time low, and local home prices soar higher than we had ever imagined. You gotta have a strategy to win! Whether you are looking to buy or to sell, you need a guide with knowledge & experience that can create a game-plan. Let my experience guide you. I offer FREE consultations to anyone that wants to chat. An easy conversation where you explain your goals and what you want to accomplish. I listen, and then I lean on my market knowledge and years of experience, to create a strategy that accomplishes your goals. If you like me, and you like my strategy, that's when I go to work making your goals a realty! Consult is free and all you have to do is call or text me to schedule! I am not mean, I don't bite, and I truly find joy in helping others accomplish your goal! If your goal is to buy now or later or to buy a $20,000 piece of land or a million dollar home I'm not picky. I love strategizing to create a path where you win! Shoot me a text or give me a call 972-533-5120

Laura Smith

Agent/Owner | Laura Smith Real Estate Team | Keller Williams e-Edge

or another way